You Can't Hide Your Lyin' Eyes

By Scott Poore, AIF, AWMA, APMA

Chief Investment Officer, Eudaimonia Group

I'm not sure if the inspiration of this week's song is fitting because of its great title or because I was just watching a Billions episode on Showtime with the Eagles hit song in the title of the episode.  I'm curious now if there really is such a thing as "Fantasy Rock Camp" as depicted in Episode 2 of Season 6, but I digress. The story behind the origin of the song was that Don Henley and Glenn Frey were sitting in their favorite bar "Dan Tanas" in L.A. As a struggling band in 1974, every night they would see beautiful women come in to their favorite watering hole with older, unattractive men at their sides. One night as they were laughing, Frey said, "Look at her, she can't even hide those lyin eyes!" And, a song was born on cocktail napkins.

I'm curious now if there really is such a thing as "Fantasy Rock Camp" as depicted in Episode 2 of Season 6, but I digress. The story behind the origin of the song was that Don Henley and Glenn Frey were sitting in their favorite bar "Dan Tanas" in L.A. As a struggling band in 1974, every night they would see beautiful women come in to their favorite watering hole with older, unattractive men at their sides. One night as they were laughing, Frey said, "Look at her, she can't even hide those lyin eyes!" And, a song was born on cocktail napkins.

"You can't hide your lyin' eyes

And your smile is a thin disguise

I thought by now you'd realize

There ain't no way to hide your lyin' eyes"

Markets seem poised to head higher, but we're not convinced the worst is over just yet. However there was some good news this week that could point to an end to the bear market sooner rather than later.

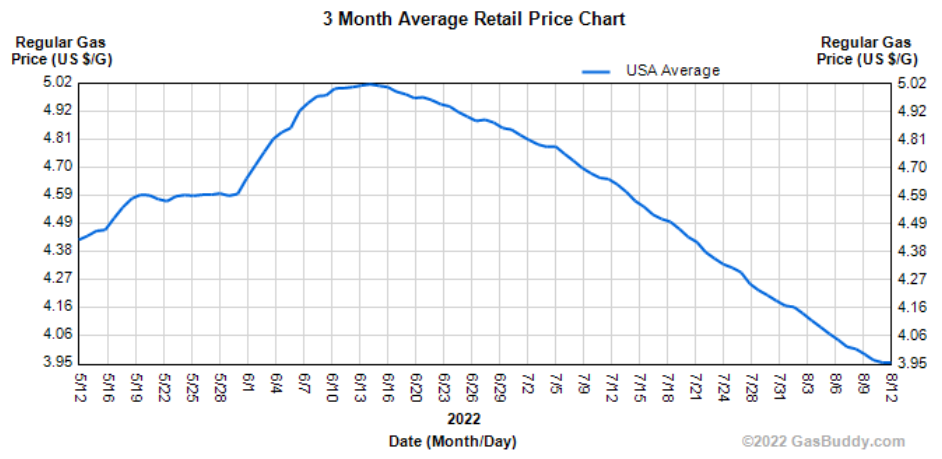

Inflation - Lying Eyes Or Forgiving Eyes? Wednesday and Thursday, we learned that inflation seemed to move lower for the first time since April.  The primary reason we're not jumping for joy just yet is that inflation declined from March to April of this year, only to head higher in May and June. So, let's see if July's good news turns into a trend before we throw a party. July CPI was flat versus a 0.2% expected increase, which caused the year-over-year number to decline from 9.1% to 8.5%. July PPI dropped 0.5% versus an expected increase of 0.2%, causing the year-over year number to fall from 11.3% the previous month to 9.8%. The largest single contributor to the decline was Energy, as gas prices have dipped from $4.81/gallon in early July to $3.95/gallon as of yesterday.

The primary reason we're not jumping for joy just yet is that inflation declined from March to April of this year, only to head higher in May and June. So, let's see if July's good news turns into a trend before we throw a party. July CPI was flat versus a 0.2% expected increase, which caused the year-over-year number to decline from 9.1% to 8.5%. July PPI dropped 0.5% versus an expected increase of 0.2%, causing the year-over year number to fall from 11.3% the previous month to 9.8%. The largest single contributor to the decline was Energy, as gas prices have dipped from $4.81/gallon in early July to $3.95/gallon as of yesterday.  We think this might have more to do with demand destruction than a shift in higher supply or greater consumption. Oil production domestically has remained consistent in June and July, with weekly production averaging between 11.9 million barrels per day to 12.1 million. Yet, both Crude Inventories and Gas Inventories increased from June to July, meaning a lack of consumption was the key change.

We think this might have more to do with demand destruction than a shift in higher supply or greater consumption. Oil production domestically has remained consistent in June and July, with weekly production averaging between 11.9 million barrels per day to 12.1 million. Yet, both Crude Inventories and Gas Inventories increased from June to July, meaning a lack of consumption was the key change.

If we dive into the Inflation numbers, we see that while energy and goods declined month-over-month, food and services increased. In fact, services increased for the 17th consecutive month to their highest level in more than two decades.  The shelter index continued to rise in July (+0.5%) and among utilities, electricity rose 11% in July. If you've received your utility bill lately, you know what I mean. Until we see some of these other areas of inflation slow, we need to wait to say the worst is over for inflation. Wages, as compared to Inflation did improve in July, but there's still a considerable gap (3.3%), which means lower income consumers are still fighting an uphill battle. Consumer Sentiment compared to Inflation also improved slightly, but like Wages, a considerable gap remains.

The shelter index continued to rise in July (+0.5%) and among utilities, electricity rose 11% in July. If you've received your utility bill lately, you know what I mean. Until we see some of these other areas of inflation slow, we need to wait to say the worst is over for inflation. Wages, as compared to Inflation did improve in July, but there's still a considerable gap (3.3%), which means lower income consumers are still fighting an uphill battle. Consumer Sentiment compared to Inflation also improved slightly, but like Wages, a considerable gap remains.

Fed Pivot - Smile Is A Thin Disguise. Since the inflation numbers came out, the futures on the Fed Funds Rate has shifted dramatically.  The jobs report last week, which was much better than expected, allowed room for the Fed to continue raising rates. As of Monday morning, the market was pricing in a 65% probability of a 75 basis point rate hike in September. Now that the market is hopeful inflation is cooling, futures are now predicting a 64% probability of a 50 basis point rate hike. Bond yields over the last few days have been all over the place, indicating that markets are uncertain as to next month's Fed rate decision.

The jobs report last week, which was much better than expected, allowed room for the Fed to continue raising rates. As of Monday morning, the market was pricing in a 65% probability of a 75 basis point rate hike in September. Now that the market is hopeful inflation is cooling, futures are now predicting a 64% probability of a 50 basis point rate hike. Bond yields over the last few days have been all over the place, indicating that markets are uncertain as to next month's Fed rate decision.  In fact, when the S&P 500 Index bottomed in mid June, bond yields started to come down. This is the opposite of what we would expect in a "risk-on" scenario. That scenario would indicate expanding corporate earnings, optimistic economic outlook, accommodative central bank policies, and speculation. And yet, investors are still buying bonds, forcing bond yields lower. This indicates that investors may not be entirely enthralled with the current rally in equities.

In fact, when the S&P 500 Index bottomed in mid June, bond yields started to come down. This is the opposite of what we would expect in a "risk-on" scenario. That scenario would indicate expanding corporate earnings, optimistic economic outlook, accommodative central bank policies, and speculation. And yet, investors are still buying bonds, forcing bond yields lower. This indicates that investors may not be entirely enthralled with the current rally in equities.

She Gets Up And Pours Herself A Strong One. The current market and economic environment probably calls for some "liquid courage" as investors are torn between "risk-on" and "risk-off" on what seems like a daily basis.  There is evidence that sentiment has shifted, but to what degree is less certain. If we look at HSBC's Market Sentiment Indicators, 12 of the 18 indicators 3 months ago were all in the "bearish" camp. Since then, 4 indicators have moved into "bullish" sentiment, 4 have remained in "bearish" sentiment, and the remaining 10 are now in "neutral" sentiment. This indicates a market that may likely trade range-bound for a little while until a catalyst moves the market in a clear direction. Equally telling is the "fear" element of our Wealth Protection Signal. It continues to trade in a rang-bound direction.

There is evidence that sentiment has shifted, but to what degree is less certain. If we look at HSBC's Market Sentiment Indicators, 12 of the 18 indicators 3 months ago were all in the "bearish" camp. Since then, 4 indicators have moved into "bullish" sentiment, 4 have remained in "bearish" sentiment, and the remaining 10 are now in "neutral" sentiment. This indicates a market that may likely trade range-bound for a little while until a catalyst moves the market in a clear direction. Equally telling is the "fear" element of our Wealth Protection Signal. It continues to trade in a rang-bound direction.  Until we see the TED Spread (fear) move below 18.9, we're not ready to call the current bear market over yet. Conversely, until the TED Spread moves above 71.8, there's no need to consider a worsening of this bear market. Our Wealth Protection Signal has only triggered once (back in May) and with the current equity rally in focus, that seems to have been a good call. Meanwhile, retail investors are back in buying mode and corporate buybacks are poised to exceed multi-decade highs.

Until we see the TED Spread (fear) move below 18.9, we're not ready to call the current bear market over yet. Conversely, until the TED Spread moves above 71.8, there's no need to consider a worsening of this bear market. Our Wealth Protection Signal has only triggered once (back in May) and with the current equity rally in focus, that seems to have been a good call. Meanwhile, retail investors are back in buying mode and corporate buybacks are poised to exceed multi-decade highs.

She'll Dress Up All In Lace And Go In Style. Underlying current market sentiment, the economic fundamentals still look weak. Jobless Claims and Continued Claims both increased last week.  It seems we have a considerable disconnect between the weekly jobs numbers and the monthly payrolls report. Initial Claims increased for the 8th consecutive week and are now at 7-month highs. Continued Claims have increased 7 of the last 11 weeks and are now at 4-month highs. Yet, somehow monthly payrolls are showing an increase of 1.8 million jobs since March.

It seems we have a considerable disconnect between the weekly jobs numbers and the monthly payrolls report. Initial Claims increased for the 8th consecutive week and are now at 7-month highs. Continued Claims have increased 7 of the last 11 weeks and are now at 4-month highs. Yet, somehow monthly payrolls are showing an increase of 1.8 million jobs since March.  This disconnect is concerting as the divergence between the Establishment Survey in the Friday's Jobs Report and the Household Survey further widened. The jobs data is key to understanding the U.S. consumer. As the consumer comprises two-thirds of U.S. GDP, if fewer consumers have jobs (i.e., steady income), there will be fewer discretionary dollars to purchase goods & services. The job market has been consistently held up as the lone indicator that the economy is in decent shape. If this piece of the pie has begun to falter, the economic picture become more dire.

This disconnect is concerting as the divergence between the Establishment Survey in the Friday's Jobs Report and the Household Survey further widened. The jobs data is key to understanding the U.S. consumer. As the consumer comprises two-thirds of U.S. GDP, if fewer consumers have jobs (i.e., steady income), there will be fewer discretionary dollars to purchase goods & services. The job market has been consistently held up as the lone indicator that the economy is in decent shape. If this piece of the pie has begun to falter, the economic picture become more dire.

___________________________________________________________________________________________________________

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.