Sorry Seems To Be The Hardest Word

By Scott Poore, AIF, AWMA, APMA

Chief Investment Officer, Eudaimonia Group

Too much money poured into the system during & post-COVID and a Fed that didn't take action last year as inflation got out of control - that's pretty much how we arrived in the current situation.  The Fed should listen to Elton John's hit song "Sorry Seems To Be The Hardest Word." The song was written by the duo of John and Bernie Taupin. However, most of their hits were written first by Taupin penning the lyrics and John writing the music to fit the lyrics. In this case, Elton was playing around on the piano in 1975 and played the main refrain and title lyric to the song. Bernie stopped him, went into a separate room, and in 5 minutes came out with the lyrics to the song. It reached number 6 on the U.S. charts in 1976.

The Fed should listen to Elton John's hit song "Sorry Seems To Be The Hardest Word." The song was written by the duo of John and Bernie Taupin. However, most of their hits were written first by Taupin penning the lyrics and John writing the music to fit the lyrics. In this case, Elton was playing around on the piano in 1975 and played the main refrain and title lyric to the song. Bernie stopped him, went into a separate room, and in 5 minutes came out with the lyrics to the song. It reached number 6 on the U.S. charts in 1976.

"It's sad, so sad

It's a sad, sad situation

And it's getting more and more absurd

It's sad, so sad

Why can't we talk it over?

Oh, it seems to me

That sorry seems to be the hardest word"

Here's what we've seeing so far this week...

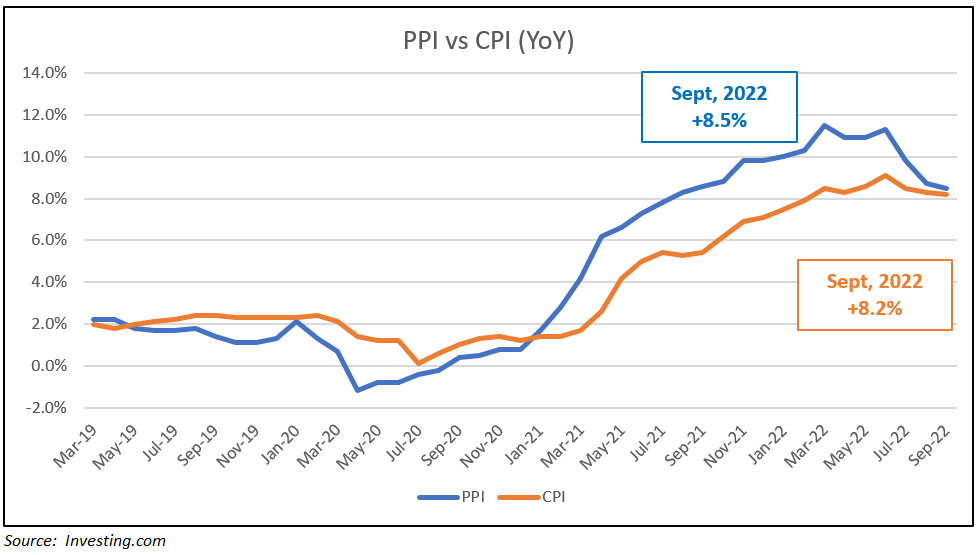

It's A Sad, Sad Situation. The inflation numbers came out this week and disappointed the market's expectations. The Producer Price  Index was higher for September (+0.4% vs +0.2% expected) and the Consumer Price Index was higher, as well (+0.4% vs +0.2% expected). While this is certainly not good news, Yet, year-over-year numbers for inflation, saw a 3rd consecutive month of declines. What we were hoping for was to see PPI drop below CPI on the year-over-year basis. As we've written about before, that typically signals the peak for inflation. Now, just because we haven't reached that mark yet does not necessarily mean the peak is out of sight. As you can see from the graph, the trend is most definitely lower. Since PPI hit a

Index was higher for September (+0.4% vs +0.2% expected) and the Consumer Price Index was higher, as well (+0.4% vs +0.2% expected). While this is certainly not good news, Yet, year-over-year numbers for inflation, saw a 3rd consecutive month of declines. What we were hoping for was to see PPI drop below CPI on the year-over-year basis. As we've written about before, that typically signals the peak for inflation. Now, just because we haven't reached that mark yet does not necessarily mean the peak is out of sight. As you can see from the graph, the trend is most definitely lower. Since PPI hit a  high of 11.5% in March, it is 3.0% lower. Similarly, since CPI hit a high of 9.1% in June, it is almost 1% lower. In addition, Wage Growth has remained fairly steady. If we had witnessed a breakout in Wage Growth over the last several months, the worry would be much higher consumption, leading to higher inflation. That has not been the case. To bolster the lack of Wage Growth, Retail Sales, while disappointing for September, have been consistent on a year-over-year basis despite higher inflation and higher interest rates. The issue now is the Fed. According to the minutes from last month's FOMC meeting, Fed members emphasized "the cost of taking too little

high of 11.5% in March, it is 3.0% lower. Similarly, since CPI hit a high of 9.1% in June, it is almost 1% lower. In addition, Wage Growth has remained fairly steady. If we had witnessed a breakout in Wage Growth over the last several months, the worry would be much higher consumption, leading to higher inflation. That has not been the case. To bolster the lack of Wage Growth, Retail Sales, while disappointing for September, have been consistent on a year-over-year basis despite higher inflation and higher interest rates. The issue now is the Fed. According to the minutes from last month's FOMC meeting, Fed members emphasized "the cost of taking too little  action to bring down inflation likely outweighed the cost of taking too much action." In other words, the Fed is willing to stick with their projected rate hikes until mid February of next year, even if that means a deeper, more lengthy recession. So despite the mess fiscal policy and Fed actions caused during and after the pandemic, we're not likely to get any help from the Fed now that inflation is beginning to recede and the economy is hanging in the balance. In fact, Fed futures on November's rate decision have risen from an 80% probability of a 75 basis point rate hike to a 98% probability.

action to bring down inflation likely outweighed the cost of taking too much action." In other words, the Fed is willing to stick with their projected rate hikes until mid February of next year, even if that means a deeper, more lengthy recession. So despite the mess fiscal policy and Fed actions caused during and after the pandemic, we're not likely to get any help from the Fed now that inflation is beginning to recede and the economy is hanging in the balance. In fact, Fed futures on November's rate decision have risen from an 80% probability of a 75 basis point rate hike to a 98% probability.

And It's Getting More And More Absurd. The market is getting whipsawed by any piece of news these days. Markets opened slightly higher on Wednesday, only to drop after the PPI print.  Markets should have reacted similarly on Thursday with a disappointing CPI print. Instead, the market took off and gained 4% on a report from the European Central Bank that it would require fewer rate hikes to tame inflation. This just fueled desperate hopes of a Fed pivot that should by now be less of a fantasy to economists. However, today, markets seem to be giving back most of those gains. At this point, it's likely that the market is looking out 6-9 months from now when the Fed stops hiking rates in February of 2023 or the Fed is forced to start lowering rates. When we look at some of the economic fundamentals,

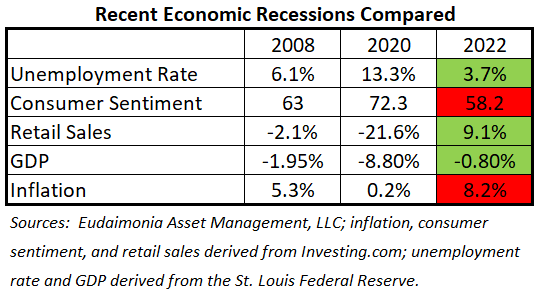

Markets should have reacted similarly on Thursday with a disappointing CPI print. Instead, the market took off and gained 4% on a report from the European Central Bank that it would require fewer rate hikes to tame inflation. This just fueled desperate hopes of a Fed pivot that should by now be less of a fantasy to economists. However, today, markets seem to be giving back most of those gains. At this point, it's likely that the market is looking out 6-9 months from now when the Fed stops hiking rates in February of 2023 or the Fed is forced to start lowering rates. When we look at some of the economic fundamentals,  there is a difference between the current recession and 2008 or 2020. Most recessions are driven by bubbles that build up and the bursting of those bubbles when job losses, bankruptcies, and payment delinquencies overtake the economic fundamentals. However, low unemployment, stable retail sales, and slightly lower GDP contrast between now and the recessions of 2008 & 2020. This dynamic can change quickly if the Fed persists. How long can consumers hold up with rising rates and current levels of inflation?

there is a difference between the current recession and 2008 or 2020. Most recessions are driven by bubbles that build up and the bursting of those bubbles when job losses, bankruptcies, and payment delinquencies overtake the economic fundamentals. However, low unemployment, stable retail sales, and slightly lower GDP contrast between now and the recessions of 2008 & 2020. This dynamic can change quickly if the Fed persists. How long can consumers hold up with rising rates and current levels of inflation?  Will companies be able to continue bringing jobs back or will job cuts become the norm? The answers to these questions is highly uncertain, which means market volatility is here to stay for a little while longer. We're less than one month from Mid-term elections, which is likely to cause trading to be a little more choppy than usual. However, we have to consider that we are 109 days away from the last Fed rate hike on February 1st of next year. The closer we get to February, the less major investment decisions we ought to make. It's worth noting that since 1974, the 12 months following Mid-term elections equities have been higher and since 1932, the year following Mid-terms was the strongest year for equities in a four year presidency.

Will companies be able to continue bringing jobs back or will job cuts become the norm? The answers to these questions is highly uncertain, which means market volatility is here to stay for a little while longer. We're less than one month from Mid-term elections, which is likely to cause trading to be a little more choppy than usual. However, we have to consider that we are 109 days away from the last Fed rate hike on February 1st of next year. The closer we get to February, the less major investment decisions we ought to make. It's worth noting that since 1974, the 12 months following Mid-term elections equities have been higher and since 1932, the year following Mid-terms was the strongest year for equities in a four year presidency.