In The Air

By Scott Poore, AIF, AWMA, APMA

Chief Investment Officer, Eudaimonia Group

Equities are having a good run as the 2nd quarter of 2023 comes to a conclusion. In fact, the S&P 500 Index is set to have its best June in four years. You can almost feel the tension in the air as Central Banks try to maintain a hawkish stance as they claim to be fighting inflation. This week's musings are inspired by the 1981 hit song "In The Air Tonight" by Phil Collins. The song was the lead single off of Collins' debut solo album, "Face Value" after departing the band Genesis. Collins claims to have offered the song to the band, but his bandmates thought is was "too simple." It looks like it was Genesis' loss, as the record is considered one of Collins' signature songs. The following entails some trivia about the song:

- The meaning behind the song became an urban myth in the late '80s, early '90s. The story goes that a man watched another man drown without offering help. Supposedly, Collins saw the man at one of his concerts and singled the man out by singing to him the words, "but I know the reason why you keep your silence up." The myth is absolutely not true, a point that Collins has made many times over the years. Collins was actually going through a divorce when he wrote the song and other than the pain of that situation, Collins has stated that he really doesn't know what the song is actually about.

- The song was popular in the U.S. and abroad, having reached . It reached #2 in the U.K. (Collins' home country) and in the U.S. in 1981. However, it re-emerged in 1984, hitting #1 in the U.S. due to its appearance on the 1983 soundtrack to "Risky Business" and being regularly used in the inaugural season of "Miami Vice" in 1984.

- One reason for the song's popularity is the famous drum break towards the end which has been described as the "sleekest, most melodramatic drum break in history." The song is listed on the "Greatest Drumming Moments" list and is listed among the "500 Greatest Songs of All Time," according to Rolling Stone.

- According to "Second Hand Songs," this hit by Phil Collins has been covered by 113 different groups over the years, including by the band Nonpoint for the 2004 film adaptation, "Miami Vice."

"Well, if you told me you were drowning, I would not lend a hand

I've seen your face before, my friend, but I don't know if you know who I am

Well, I was there and I saw what you did, I saw it with my own two eyes

So you can wipe off that grin, I know where you've been

It's all been a pack of lies

And I can feel it coming in the air tonight, oh Lord

Well, I've been waiting for this moment for all my life, oh Lord

I can feel it coming in the air tonight, oh Lord

Well, I've been waiting for this moment for all my life, oh Lord, oh Lord"

Here's what we've seen so far this week...

Urban Myths. I freely admit that I fell for the urban myth surrounding the song, "In The Air Tonight" as a young teenager, until I reached a ripe old age of 18 when I finally asked the question,  "If Phil Collins wrote a song about a man he saw fail to help another drowning man, doesn't that mean that Collins also failed to help the drowning man?" I quickly learned the valuable lesson of failed myths. It's easy to fall in line with believing a myth when so many purport the myth. When it comes to Central Banks, there are many myths being purported these days. This week, at the ECB Forum on Central Banking, Fed Chairman Powell denied that government spending and the Fed's Quantitative Easing during the pandemic contributed to inflation rising in 2021 and 2022. Really?

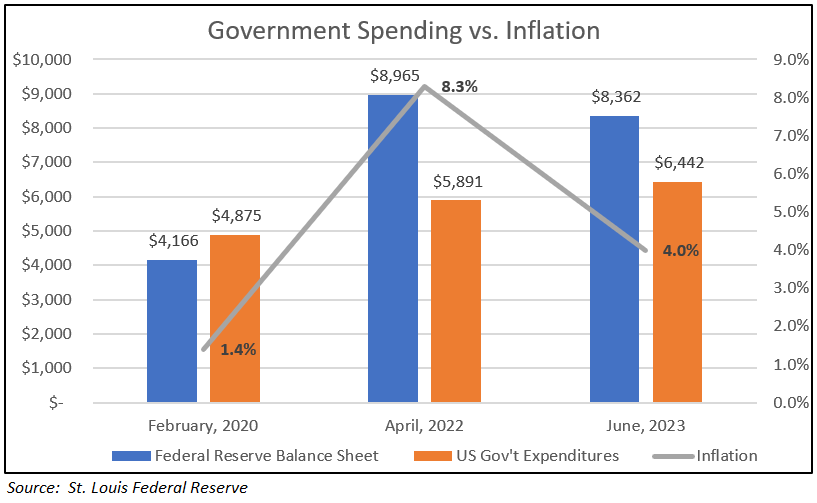

"If Phil Collins wrote a song about a man he saw fail to help another drowning man, doesn't that mean that Collins also failed to help the drowning man?" I quickly learned the valuable lesson of failed myths. It's easy to fall in line with believing a myth when so many purport the myth. When it comes to Central Banks, there are many myths being purported these days. This week, at the ECB Forum on Central Banking, Fed Chairman Powell denied that government spending and the Fed's Quantitative Easing during the pandemic contributed to inflation rising in 2021 and 2022. Really?  Let's look at government spending and the Fed's Balance Sheet prior to COVID and following. In February 2020, the Fed's Balance Sheet had shrunk from a peak of nearly $4.5 trillion to $4.1 trillion. Government Spending had slowly risen to $$4.8 trillion by that time. Inflation, meanwhile, was at +1.4%. When the pandemic broke out, both government spending and the Fed's Balance Sheet exploded.

Let's look at government spending and the Fed's Balance Sheet prior to COVID and following. In February 2020, the Fed's Balance Sheet had shrunk from a peak of nearly $4.5 trillion to $4.1 trillion. Government Spending had slowly risen to $$4.8 trillion by that time. Inflation, meanwhile, was at +1.4%. When the pandemic broke out, both government spending and the Fed's Balance Sheet exploded.  The Fed's Balance Sheet more than doubled with asset purchases by April of 2022 and government spending, which peaked at $8.1 trillion in March of 2021, had come down to $5.8 trillion by April of 2022. At the same time, inflation skyrocketed to +8.3%. In March of 2021, when government spending peaked, the American Rescue Plan was signed by President Biden which added another $1.9 trillion in spending - $350 billion to state & local governments, $160 billion in additional (unnecessary) COVID stimulus, and $86 billion for special interest groups.

The Fed's Balance Sheet more than doubled with asset purchases by April of 2022 and government spending, which peaked at $8.1 trillion in March of 2021, had come down to $5.8 trillion by April of 2022. At the same time, inflation skyrocketed to +8.3%. In March of 2021, when government spending peaked, the American Rescue Plan was signed by President Biden which added another $1.9 trillion in spending - $350 billion to state & local governments, $160 billion in additional (unnecessary) COVID stimulus, and $86 billion for special interest groups.  Since then, government spending has edged slightly higher with infrastructure projects, while the Fed's Balance Sheet has come down to $8.3 trillion. Now that much of the excess savings from the pandemic has eroded, inflation has been cut by more than half and is now at +4.0%. Still think there is no correlation between government spending and inflation? The other prevailing myth when it comes to Central Banks is their repeated claims that they must continue to battle inflation.

Since then, government spending has edged slightly higher with infrastructure projects, while the Fed's Balance Sheet has come down to $8.3 trillion. Now that much of the excess savings from the pandemic has eroded, inflation has been cut by more than half and is now at +4.0%. Still think there is no correlation between government spending and inflation? The other prevailing myth when it comes to Central Banks is their repeated claims that they must continue to battle inflation.  However, if we look at the top 5 global economies - U.S., China, Japan, Germany, & the U.K. - a continued aggressive (or hawkish) battle against inflation appears to be over. The top 5 economies, with the exception of Germany, appear to have witnessed a peak for inflation in 2022 and steady declines in 2023. So, what are Central Banks battling? When it comes to the U.S. economy, inflation has cratered and it's showing up in all of the data. The latest survey of manufacturing conducted by the Dallas Fed, shows that prices of raw materials are near lows not seen since 2015. Today's release of the May PCE Price Index also confirms that inflation is cratering. The expected number was +4.6%, year-over-year, but the number actually came in at 3.8%. In addition, last month's number was revised lower from 4.4% to 4.3%. Even the Fed's favorite measure of inflation has come down to 3.8% from a peak of 6.8% 12 months ago. At this point, we have to ask ourselves, what inflation is the Fed still fighting?

However, if we look at the top 5 global economies - U.S., China, Japan, Germany, & the U.K. - a continued aggressive (or hawkish) battle against inflation appears to be over. The top 5 economies, with the exception of Germany, appear to have witnessed a peak for inflation in 2022 and steady declines in 2023. So, what are Central Banks battling? When it comes to the U.S. economy, inflation has cratered and it's showing up in all of the data. The latest survey of manufacturing conducted by the Dallas Fed, shows that prices of raw materials are near lows not seen since 2015. Today's release of the May PCE Price Index also confirms that inflation is cratering. The expected number was +4.6%, year-over-year, but the number actually came in at 3.8%. In addition, last month's number was revised lower from 4.4% to 4.3%. Even the Fed's favorite measure of inflation has come down to 3.8% from a peak of 6.8% 12 months ago. At this point, we have to ask ourselves, what inflation is the Fed still fighting?

In The Air. We've all been waiting for the moment when a new bull market might show its face. There are plenty of signs that it's here, but that doesn't mean the sailing will always be smooth.  Prior to June 16th, equities had been on a run. After a brief respite last week, equities seem to have regained some steam this week. However, there could be some bumpy trading ahead, more to do with allocations than sentiment. Equities have been on such a run when compared to Fixed Income that many pension funds are likely to be forced to rebalance in the coming days. In fact, we might have already seen some trading in regard to this allocation shift. According to Goldman Sachs, some $26 billion in US equities may be rebalanced into fixed income as pensions have to meet their mandates.

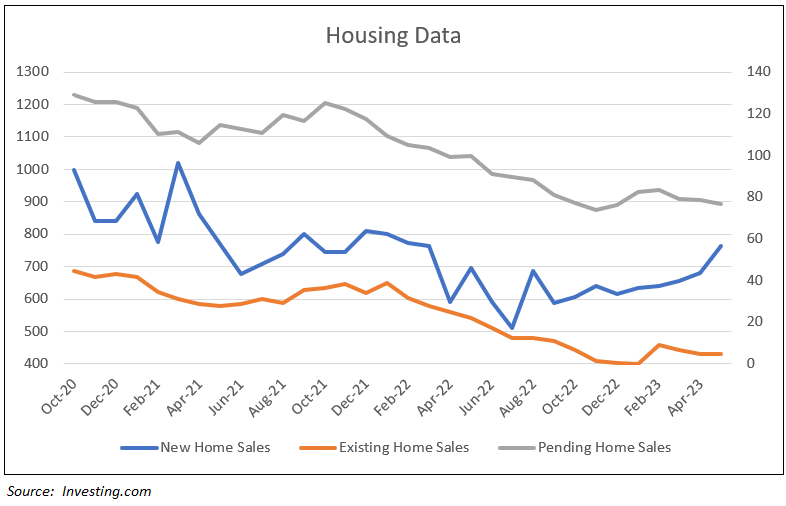

Prior to June 16th, equities had been on a run. After a brief respite last week, equities seem to have regained some steam this week. However, there could be some bumpy trading ahead, more to do with allocations than sentiment. Equities have been on such a run when compared to Fixed Income that many pension funds are likely to be forced to rebalance in the coming days. In fact, we might have already seen some trading in regard to this allocation shift. According to Goldman Sachs, some $26 billion in US equities may be rebalanced into fixed income as pensions have to meet their mandates.  Over the last quarter, equities have out-performed fixed income by more than 700 basis points. Housing data was better in the month of May. Building Permits, Mortgage Applications, New Home Sales, and Existing Home Sales were all higher for the month. Pending Home Sales did disappoint, but have still not dropped down to the low level reached in November of last year. The University of Michigan's Consumer Sentiment for June came out this morning at 64.4, which was higher than forecast and much higher than last month's reading of 59.2. Personal Income came in higher for the April reading, while Personal Spending was lower than expected, but still higher than March. As Summer vacations begin, we'll see if the June reading for Personal Spending improves. However, with a healthy consumer and a return of more than 5% slated for equities in June, the prospect of a solid 2nd half for 2023 remains a strong possibility.

Over the last quarter, equities have out-performed fixed income by more than 700 basis points. Housing data was better in the month of May. Building Permits, Mortgage Applications, New Home Sales, and Existing Home Sales were all higher for the month. Pending Home Sales did disappoint, but have still not dropped down to the low level reached in November of last year. The University of Michigan's Consumer Sentiment for June came out this morning at 64.4, which was higher than forecast and much higher than last month's reading of 59.2. Personal Income came in higher for the April reading, while Personal Spending was lower than expected, but still higher than March. As Summer vacations begin, we'll see if the June reading for Personal Spending improves. However, with a healthy consumer and a return of more than 5% slated for equities in June, the prospect of a solid 2nd half for 2023 remains a strong possibility.

Here's Phil's major hit song for your listening pleasure...

___________________________________________________________________________________________________________

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.