Has The Market Stopped Listening To The Fed (Part Deux)

By Scott Poore, AIF, AWMA, APMA

Chief Investment Officer, Eudaimonia Group

This week has been a little uninspiring. Markets are down a little more than 1%, with momentum/growth names giving up some of the gains over the last few weeks.  As such, there wasn't much I could find to inspire me, so we're just calling this week's musings "Part Deux" of last week's post. The 1993 movie, "Hot Shots, Part Deux" was a sequel to the 1991 spoof on "Top Gun." In part Deux, the movie the studios were spoofing was "Rambo." To be honest, there's not much really redeeming about the movie. The budget was $25 million and it only grossed $38 million in the U.S. It was much more successful overseas, grossing about $95 million. However, the movie's title alone serves our purposes for this week's post.

As such, there wasn't much I could find to inspire me, so we're just calling this week's musings "Part Deux" of last week's post. The 1993 movie, "Hot Shots, Part Deux" was a sequel to the 1991 spoof on "Top Gun." In part Deux, the movie the studios were spoofing was "Rambo." To be honest, there's not much really redeeming about the movie. The budget was $25 million and it only grossed $38 million in the U.S. It was much more successful overseas, grossing about $95 million. However, the movie's title alone serves our purposes for this week's post.

Here's what we've seen this week...

Asked and Answered. Last week we ended the musings by speculating that perhaps investors might fall back into the same pattern of focusing on every breath from the Fed. That turned out to be the case this week.  Fed members, including Chairman Powell, were out in force this week and picked up the hawkish language where they left off last week. This time, however, the market was listening and equities have moved lower overall this week. Most Fed speakers reinforced the idea that it will take "longer" for the Fed to slow the pace of price increases. Some speakers countered that saying the Fed should steer "more deliberately" from here due to lagged effects of policy.

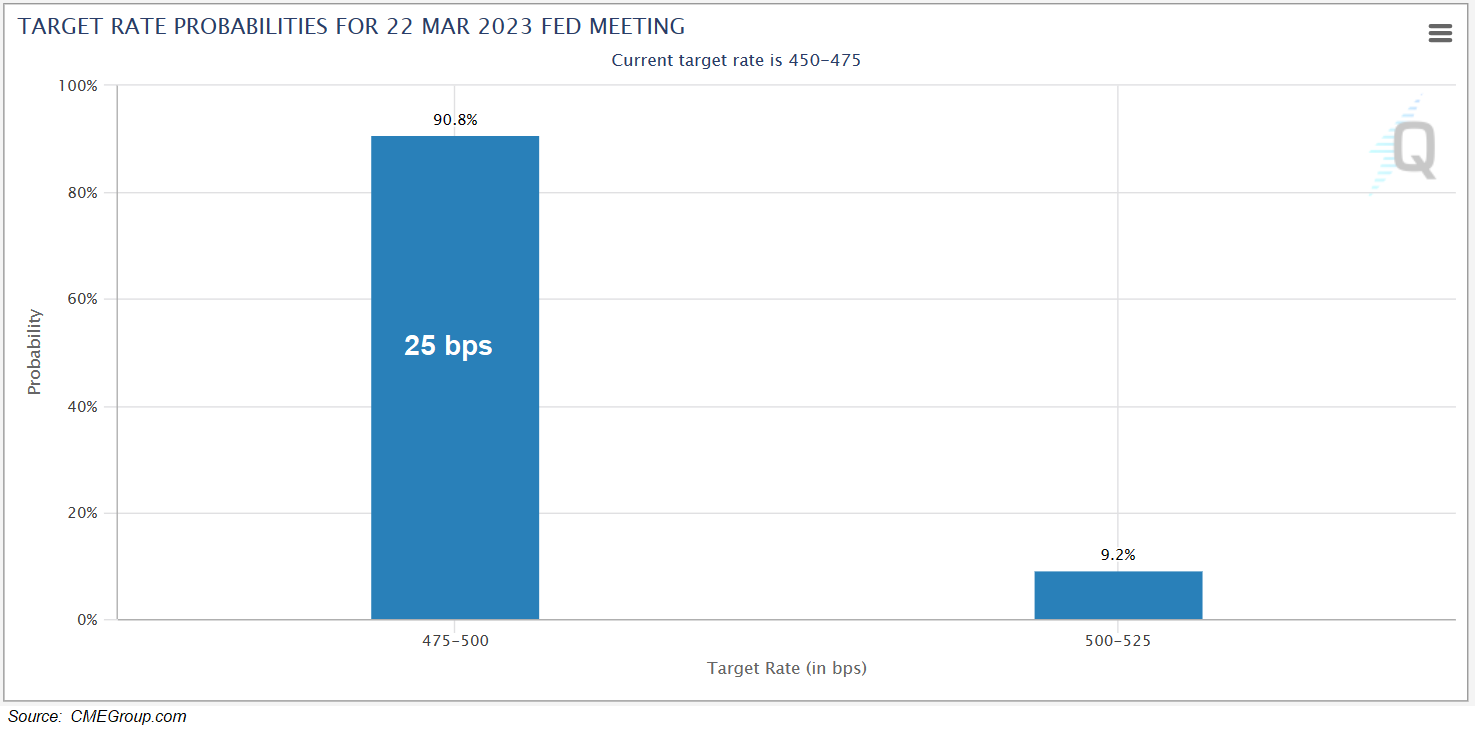

Fed members, including Chairman Powell, were out in force this week and picked up the hawkish language where they left off last week. This time, however, the market was listening and equities have moved lower overall this week. Most Fed speakers reinforced the idea that it will take "longer" for the Fed to slow the pace of price increases. Some speakers countered that saying the Fed should steer "more deliberately" from here due to lagged effects of policy.  So far, the markets are pricing in another 25 basis point rate hike next month. Most of the voting members of the FOMC are in the hawkish camp, which means 25 bps next month could be all but certain. However, inflation has peaked and even some speakers (namely Barkin on Thursday) acknowledged as much. We'll get CPI and PPI data next week for the month of January and both are expected to show another decline, which would market the 7th consecutive decline for both inflation measures on a year-over-year basis. This week, after announcing their 4th quarter results, the CFO of Pepsico noted that they were through with price increases for the year. The Fed is going to find being more "deliberate" with rate decisions difficult going forward.

So far, the markets are pricing in another 25 basis point rate hike next month. Most of the voting members of the FOMC are in the hawkish camp, which means 25 bps next month could be all but certain. However, inflation has peaked and even some speakers (namely Barkin on Thursday) acknowledged as much. We'll get CPI and PPI data next week for the month of January and both are expected to show another decline, which would market the 7th consecutive decline for both inflation measures on a year-over-year basis. This week, after announcing their 4th quarter results, the CFO of Pepsico noted that they were through with price increases for the year. The Fed is going to find being more "deliberate" with rate decisions difficult going forward.

Still Room For A Soft Landing? Investors still have much room for hope as there are some green shoots in the economy.  The mortgage market is showing signs of recovery as weekly applications were up 7.4% this week, after taking a breather last week. In fact, after suffering substantial drop off last year as rates were rising, mortgage applications have been up 6 of the last 8 weeks as the 30-year mortgage rate is down to 6.1% from the high of 7.1% in October of last year. The Mortgage Market Index tracked by the Mortgage Bankers Association of America has improved in 4 of the last 5 weeks, indicating maybe a bottom has been established.

The mortgage market is showing signs of recovery as weekly applications were up 7.4% this week, after taking a breather last week. In fact, after suffering substantial drop off last year as rates were rising, mortgage applications have been up 6 of the last 8 weeks as the 30-year mortgage rate is down to 6.1% from the high of 7.1% in October of last year. The Mortgage Market Index tracked by the Mortgage Bankers Association of America has improved in 4 of the last 5 weeks, indicating maybe a bottom has been established.  The University of Michigan's Consumer Sentiment index came out this morning at the highest level we've seen since January of last year, when the Bear Market began. If the consumer holds steady through next month's FOMC meeting, the U.S. economy could very well achieve a "soft landing." Meanwhile, corporate buybacks remain steady, as the amount of share buybacks has already exceeded the amount in both the 3rd & 4th quarters of 2022. This could help fuel markets this year. However, the VIX (volatility) has recently picked up and is threatening to rise above the 50-day moving average, which it has successfully stayed below since the end of October last year. Another drop in inflation revealed next week could lift markets, but there are more Fed speakers next week, as well. They may try to keep equity markets at bay for a 2nd consecutive week if investors buy into their hawkish language.

The University of Michigan's Consumer Sentiment index came out this morning at the highest level we've seen since January of last year, when the Bear Market began. If the consumer holds steady through next month's FOMC meeting, the U.S. economy could very well achieve a "soft landing." Meanwhile, corporate buybacks remain steady, as the amount of share buybacks has already exceeded the amount in both the 3rd & 4th quarters of 2022. This could help fuel markets this year. However, the VIX (volatility) has recently picked up and is threatening to rise above the 50-day moving average, which it has successfully stayed below since the end of October last year. Another drop in inflation revealed next week could lift markets, but there are more Fed speakers next week, as well. They may try to keep equity markets at bay for a 2nd consecutive week if investors buy into their hawkish language.

___________________________________________________________________________________________________________Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.