Fed Teetering On The Precipice

By Scott Poore, AIF, AWMA, APMA

Chief Investment Officer, Eudaimonia Group

The Fed and Chairman Powell are living dangerously these days as they play with investors' emotions in an extremely expensive game. If you take the Fed Hawkish language last week and this week and sprinkle in a little external drama, you have yourself a market pullback.

"Tommy used to work on the docks

Union's been on strike, he's down on his luck

It's tough, so tough

Gina works the diner all day

Working for her man, she brings home her pay for love

Mmm, for love

She says, 'We've gotta hold on to what we've got

It doesn't make a difference if we make it or not

We got each other, and that's a lot for love

We'll give it a shot'

Whoa, we're half way there

Oh-oh, livin' on a prayer

Take my hand, we'll make it, I swear

Oh-oh, livin' on a prayer"

The Fed is living on a prayer, and we'll tell you why...

Fed Hawk Down On His Luck? The Fed and Chairman Powell have been playing the double-speak game for so long, it was only a matter of time before their luck ran out.  This week, Powell spoke in his typical vague tongue to try to keep markets under control and prevent a bullish cycle from taking hold. On Tuesday, before the Joint Economic Committee in D.C., he commented that while inflation has "moderated somewhat" it remains well above the Fed's target of 2% (as measured against the PCE Index +5.4%). He then went on to say, ".... If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes... The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done." Equities promptly sold off 1.5% on Tuesday and the yield on the 2-year Treasury spiked 18 basis points as Fed Implied Futures increased for a March 50 basis point rate hike versus the previously favored 25 basis point hike. Markets calmed the following day as Chairman Powell finished his comments before the committee by stating, "If — and I stress that no decision has been made on this — but if the totality of the data were to indicate that faster tightening is warranted, we’d be prepared to increase the pace of rate hikes.” Per usual, Powell provided hope for the markets that faster tightening is not yet warranted by the data. Then, on Thursday, downward pressure that was already present deepened.

This week, Powell spoke in his typical vague tongue to try to keep markets under control and prevent a bullish cycle from taking hold. On Tuesday, before the Joint Economic Committee in D.C., he commented that while inflation has "moderated somewhat" it remains well above the Fed's target of 2% (as measured against the PCE Index +5.4%). He then went on to say, ".... If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes... The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done." Equities promptly sold off 1.5% on Tuesday and the yield on the 2-year Treasury spiked 18 basis points as Fed Implied Futures increased for a March 50 basis point rate hike versus the previously favored 25 basis point hike. Markets calmed the following day as Chairman Powell finished his comments before the committee by stating, "If — and I stress that no decision has been made on this — but if the totality of the data were to indicate that faster tightening is warranted, we’d be prepared to increase the pace of rate hikes.” Per usual, Powell provided hope for the markets that faster tightening is not yet warranted by the data. Then, on Thursday, downward pressure that was already present deepened.

- Financial stocks came under pressure as SVB Financial Group, parent to Silicon Valley Bank which is a high profile bank in the Venture Capital space, experienced significant losses due to poor investments and a plan to restructure. That spilled over to a handful of other banks with associated investments of SVB.

- Then, in a perfectly-timed release, the Biden administration unveiled its latest budget proposal that calls for an increase in tax rates (28% Corporate Tax from 21%, 25% minimum tax on the wealthy, and a 4% tax on stock buybacks from 1%).

- If that were not enough, there were reports on the geopolitical landscape that Russia is planning a "large-scale provocation" with Ukraine along the Belarus border.

The game the Fed has been playing to try and keep equities from running just turned against them as it has now coincided with news placing more downward pressure on markets.

We're More Than "Half Way There." Since Powell's poorly timed comments on Tuesday, Fed Rate Hike expectations have cooled and bonds have responded in-kind. The reality is, the market knows that there is light at the end of the tunnel.  Whether it's March, May, or June, rate hikes are soon to end. Powell knows this and is trying to keep equities from rising substantially to keep the "wealth effect" from adding to inflation. We've written about the "wealth effect" before, so I won't go into a deeper dive on the theory. What we have seen the futures on March's rate hike decision change drastically over the past 7 days. As of last week, futures were solidly in the favor of a 25 basis point hike with a 70%+ probability. On Wednesday, those odds flipped with a 68% probability of a 50 basis point rate hike, and as previously stated, the yield on the 2-year Treasury rose accordingly. As of today, those odds are now back down and slightly in favor of a 25 bps rate hike.

Whether it's March, May, or June, rate hikes are soon to end. Powell knows this and is trying to keep equities from rising substantially to keep the "wealth effect" from adding to inflation. We've written about the "wealth effect" before, so I won't go into a deeper dive on the theory. What we have seen the futures on March's rate hike decision change drastically over the past 7 days. As of last week, futures were solidly in the favor of a 25 basis point hike with a 70%+ probability. On Wednesday, those odds flipped with a 68% probability of a 50 basis point rate hike, and as previously stated, the yield on the 2-year Treasury rose accordingly. As of today, those odds are now back down and slightly in favor of a 25 bps rate hike.  As such, the 2-year treasury yield has declined from a 5.08% peak on Tuesday to 4.65% as of this morning. You see, Powell knows that if he were to hike rates more by 50 bps after the downward shift in hikes that began in 2022, markets would descend into a tailspin and the economy would likely follow. He's playing the word game between hawkish and dovish comments to keep equities at bay. The S&P 500 Index rallied nearly 2.5% last week, so he came out hawkish this week. But, what changed between last week and this week? Not much from an economic perspective (more on that in a minute). According to Michael Lebowitz at RIA Advisors, the lag effect from all of the previous rate hikes, while immediate, also could extend out as far as the end of 2024. Powell created a short-term panic over the possibility of a 50 basis point rate hike, but even he knows that the difference between a 50 bps and 25 bps hike would be severely detrimental to economic growth akin to the Richter Scale difference between a 3.0 earthquake and a 4.0 earthquake. In other words, he's likely bluffing or incredibly ignorant. I'd advocate for the former.

As such, the 2-year treasury yield has declined from a 5.08% peak on Tuesday to 4.65% as of this morning. You see, Powell knows that if he were to hike rates more by 50 bps after the downward shift in hikes that began in 2022, markets would descend into a tailspin and the economy would likely follow. He's playing the word game between hawkish and dovish comments to keep equities at bay. The S&P 500 Index rallied nearly 2.5% last week, so he came out hawkish this week. But, what changed between last week and this week? Not much from an economic perspective (more on that in a minute). According to Michael Lebowitz at RIA Advisors, the lag effect from all of the previous rate hikes, while immediate, also could extend out as far as the end of 2024. Powell created a short-term panic over the possibility of a 50 basis point rate hike, but even he knows that the difference between a 50 bps and 25 bps hike would be severely detrimental to economic growth akin to the Richter Scale difference between a 3.0 earthquake and a 4.0 earthquake. In other words, he's likely bluffing or incredibly ignorant. I'd advocate for the former.

We've Gotta To Hold On To What We've Got. And, what we've got is data. A strong jobs number this morning showed that 311,000 more jobs were added to the labor market in February.  That's 106,000 more than expected. However, the Unemployment Rate inched higher in February from 3.4% to 3.6%. We've seen layoffs announced in the tech sector and that was borne out in the government's report. The unemployment rate increased for the 1st time since November of 2022. This is something we'll need to watch as we deal with Powell's double-speak.

That's 106,000 more than expected. However, the Unemployment Rate inched higher in February from 3.4% to 3.6%. We've seen layoffs announced in the tech sector and that was borne out in the government's report. The unemployment rate increased for the 1st time since November of 2022. This is something we'll need to watch as we deal with Powell's double-speak.  At the same time, Job Openings were higher than expected in February and remain elevated, meaning that if someone is laid off, there are at least 4-5 jobs available for that individual. This is good for the economy, because as we've repeated pointed out, if the consumer has a job and has money to spend, the economy grows. Mortgage applications saw a nice bounce-back (+7.4%) after suffering three weeks of declines. The Fed's own National Financial Conditions Index points to steady financial conditions as of last week's close that does not signal a concern as of yet.

At the same time, Job Openings were higher than expected in February and remain elevated, meaning that if someone is laid off, there are at least 4-5 jobs available for that individual. This is good for the economy, because as we've repeated pointed out, if the consumer has a job and has money to spend, the economy grows. Mortgage applications saw a nice bounce-back (+7.4%) after suffering three weeks of declines. The Fed's own National Financial Conditions Index points to steady financial conditions as of last week's close that does not signal a concern as of yet.

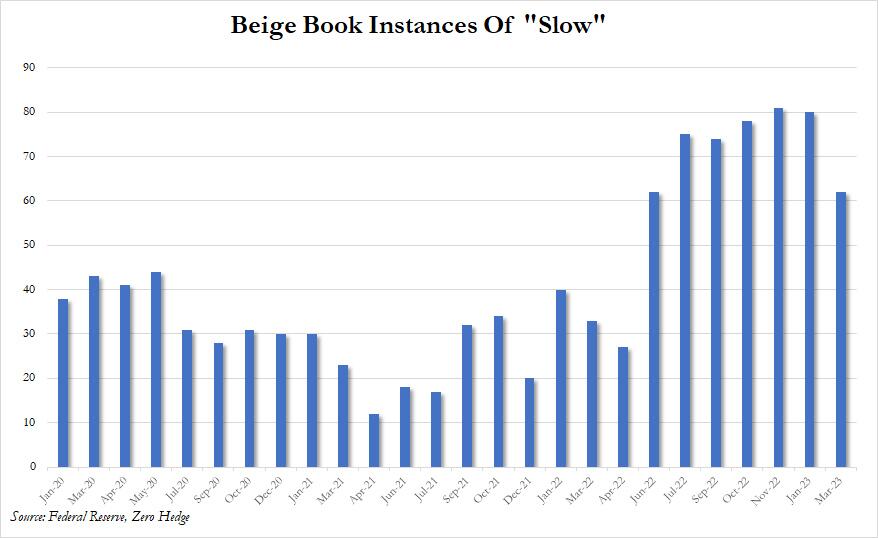

In addition, this month's Beige Book release by the Fed showed fewer instances in the survey to both "inflation" and "slow" growth. In spite of this positive data, much is being made of the recent financial sector news and possible "contagion." First, no one, and I mean NO ONE, can predict the next contagion event or "black swan" as it were. Second, the size of the U.S. banking system (more than $22 trillion) is large enough to absorb the hit to a Venture Capital bank in SVB ($200 billion) (as of this writing, the California Department of Financial Protection and Innovation has shut down the SVB Bank and all insured depositors will have full access to their deposits). We will be watching the markets and the data carefully, but as some have observed, the Fed Chairman should wield his Fed Funds stick carefully going forward as it becomes increasingly dangerous to swing.

___________________________________________________________________________________________________________Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.